From regional bank to becoming the second largest financial institution in Mexico.

Main growth drivers:

- Initial growth was driven by acquisitions of smaller regional players in order to achieve a nationwide footprint.

- Subsequent growth was still mostly inorganic, acquiring other institutions to become a financial group and achieve revenue diversification.

- From 2014 onwards, growth has been mainly organic, focusing on investing in IT, on executing a customer-centric strategy aimed at improving product quality, customer service and initiating our digital transformation.

These strategies have helped GFNORTE to become the second largest financial group in Mexico.

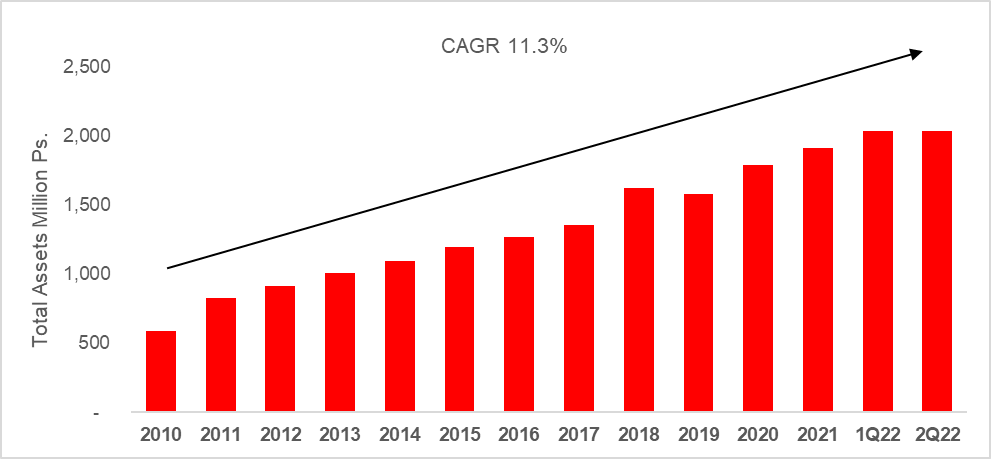

Total Assets Growth

Customer Growth

- GFNorte has diversified its customer base, now serving more than 20 million customers across different business lines.

- Through its revenue diversification efforts, GFNorte now concentrates slightly less than 50% of its client base in the bank, and the rest is spread across different businesses:

- Bank: 11,418,359.

- Pension Fund (Afore XXI Banorte): 8,630,719.

- Insurance: 10,244,536.

- Annuities: 190,607.

Infrastructure Growth

Our customer-centric strategy entailed important technological and infrastructure changes for the group, among the most important ones:

Branch Redesign

- In an effort to improve customer service and cross-selling rates, in 2015 we launched a branch redesign program which includes changes in branch layout, design and technology.

- New branches are equipped with more ATMs where customers can make simple transactions faster, such as balance inquiries, deposits, withdrawals, credit card and services payments, and new product hiring.

- Branch personnel can now spend more time on onboarding new customers and cross-selling to existing ones.

- New branches have approximately 15% lower operating cost per year than traditional ones.

IT Redesign

- Considerable resources were invested to redesign our IT core infrastructure, with the following important results:

- Create a simpler core IT architecture, enabling a shorter time to market and improved customer service.

- Achieve a multi-channel product delivery: provide a standard, consistent product delivery across all product channels: branches, ATMs, Web portal, Mobile App, and Customer Contact Center.

- Gather data across all product channels and create a central data repository with valuable customer data.

- Build an analytics team to interpret, and use data to become much more efficient cross-sellers.

- Enhance our mobile app, and work towards becoming a 100% digital bank.

Competitive Advantages

- Stable, low cost retail funding resulting from a broad and loyal customer deposit base: 70% demand; 30% time deposits.

- Savvy government lending origination team, with particular expertise in government infrastructure lending.

- Implementation of Net Promoter Score (NPS) to evaluate customer satisfaction and identify pain points.

- NPS has been implemented across all product lines, and all channels, generating very valuable feedback which we use to improve products, systems, and processes, to enhance customer satisfaction.

- Underpenetrated customer base, with ample potential for cross selling.

- Best-in-class analytics infrastructure which has contributed to a significant revenue enhancement for the group through several initiatives:

- Customer segmentation project – increased sales effectiveness by addressing the right customer with the right product.

- Use multi-channel approach to direct specific promotions to the right customers across all channels.

- Increased credit card cross selling by offering pre-approved cards to the right customer base.

- Campaigns to increase credit card activation rates and credit line utilization.

- Campaigns to incentivize customer deposits.

- Campaigns to increase customer retention by sending customized promotions on early signs of potential customer churn, such as lower credit card utilization or lower than normal checking account transactions.

20/20 Plan: GFNorte’s strategy towards 2020

In 2015 we delineated an ambitious set of goals which will drive our growth and lead us towards becoming the Best Financial Group in Mexico, for Mexicans.

Even though in 2020 our results reflected the impact of the COVID-19 pandemic, the dedication and coordinated work of our entire team allowed us to achieve these goals in many areas, one year earlier than promised.